Low Expectation, High Optionality – The UK Opportunity

Harry Fraser

Partner | Portfolio ManagerHarry joined OP in August 2011. He was previously employed by Herald Investment Management as a research analyst covering the media sector for a total of 5 years. He graduated from Newcastle University, and is a CFA Charterholder. He manages global smaller companies portfolios, and contributes to the overall investment selection.

Recent publications

In The Intelligent Investor, Benjamin Graham introduced investors to Mr Market: a volatile business partner whose emotional extremes create opportunity for those able to remain rational. At moments of euphoria, Mr Market demands absurd prices. At moments of despair, he offers sound businesses at prices that imply permanent impairment. Few major equity markets today look as though they are more firmly in the grip of Mr Market’s pessimism than the United Kingdom.

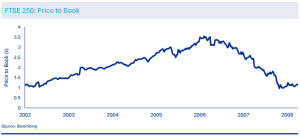

Over the past two decades, the UK has transitioned from a favoured destination for capital to one broadly shunned by global investors. In the early 2000s, optimism was pervasive. A prolonged period of low inflation, steady growth, and financial deregulation fostered confidence that the UK had somehow tamed the economic cycle. Valuations expanded dramatically. As highlighted in the chart below, the FTSE 250, a rough proxy for domestic UK businesses, rose from around one times book value to over three times in the five years following 2002. Then came the reckoning.

The global financial crisis exposed the fragility of a growth model overly dependent on leverage and finance. The UK became the first developed economy to suffer a modern retail bank run at Northern Rock, a psychological shock that marked the end of complacency. What followed was not a sharp, cathartic downturn, but a prolonged period of stagnation. Lending contracted, investment slowed, and valuations collapsed. The price-to-book ratio of UK equities fell by more than 70% from peak levels.

Crucially, this was not a short cycle. A decade of austerity eroded public confidence and constrained growth. Political instability: Scottish independence, Brexit, revolving prime ministers, cemented the UK’s reputation as “uninvestable.” By the time inflation surged and interest rates rose post-COVID, the UK was already trading at a deep valuation discount to global peers.

And yet, it is precisely here, after disappointment has lingered long enough to feel permanent, that long-term opportunity tends to emerge.

Valuation that Assumes Failure

UK equities today are priced as though mediocrity, or worse, is inevitable. Across market caps, valuation multiples remain meaningfully below global averages, not only on earnings but on tangible asset value. This is not a market priced for excellence; it is a market priced for disappointment. History suggests that when expectations are low, merely adequate outcomes can drive attractive returns.

Capital Discipline in a World of Excess

One of the quiet but important developments in the UK market has been a renewed focus on capital allocation. Share buybacks have accelerated meaningfully in recent years, reflecting both conservative balance sheets and management teams unconvinced that their own equity is fairly valued. When companies choose to repurchase shares at depressed valuations, they effectively arbitrage Mr Market’s pessimism on behalf of long-term owners.

This behaviour contrasts sharply with periods of market exuberance, when capital is often squandered on overpriced acquisitions or marginal projects. Today’s UK corporate landscape is shaped more by restraint than excess.

Global Businesses, Local Prices

A common misconception is that investing in the UK is a bet on the UK economy. In reality, a significant portion of UK-listed companies generate revenues globally, often in dollars or euros, while being priced as if they were purely domestic, structurally impaired businesses. This disconnect allows investors to buy international earnings streams at local-market discounts.

The Asymmetry is the Opportunity

Perhaps the most compelling reason to consider the UK today is asymmetry. The prevailing narrative already discounts a great deal of bad news. Political dysfunction, low productivity, and weak growth are well understood and embedded in prices. What is not priced in is any positive surprise: policy stability, modest productivity improvement, or simply time passing without catastrophe.

As Graham observed, the market’s job is not to instruct but to serve. Today, Mr Market’s mood towards the UK is deeply pessimistic. For patient investors with a long horizon, that pessimism is not a warning sign, it is the opportunity.

Accessing the Opportunity

At Oldfield Partners, we are stock pickers, looking to acquire companies that will deliver us above average returns. We do not make calls on whether a particular region or sector will outperform; however, we do believe in the concept of ‘fishing where the fish are,’ which has resulted in many ideas in our strategies coming from the UK market.

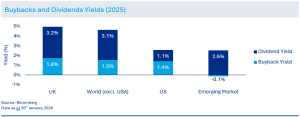

We find large companies like Shell and Lloyds; mid-sized businesses, Whitbread and Jet2; and small companies, JD Wetherspoon and Moonpig. They all trade at discounts to comparable companies in other countries and are returning to shareholders, through buybacks and dividends, over 6% of their market caps.

United Kingdom

United Kingdom United States

United States Canada

Canada