Investing in the European automotive industry in an age of disruption

Christoph Ohm

Portfolio ManagerChristoph joined OP in August 2015. He previously worked as an analyst at Marlborough Partners, providing financing advice to private equity firms. Before that, he worked in the valuation team at Duff & Phelps. He graduated from Aston Business School and Free University of Berlin, and is a CFA Charterholder. He co-manages the international portfolios, and contributes to the overall investment selection.

The automotive industry is undergoing a profound transformation, driven by rising Chinese competition and mounting margin pressure. This analysis explores the challenges facing European automotive companies and outlines how we at Oldfield Partners are investing in the current environment. Our approach focuses on more resilient supply-chain businesses and assesses the emerging fightback from incumbent manufacturers.

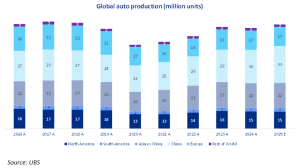

Global auto sales peaked at 94 million units in 2017. Estimates for 2025 stand at around 91 million, with higher financing costs and prices continuing to weigh on affordability. Expectations point to low single-digit annual volume growth in the years ahead, with a return to peak levels by 2028, supported by fleet ages that are already at historically high levels. The industry should also benefit from a moderation in cost inflation and interest rates. The moderate decline in sales over recent years masks a dramatic shift in who is buying the car and who is producing it. Since 2017, car sales in Europe have fallen by around 10%, while the rest of the world is down only 1%. European manufacturers have suffered more than these sales figures suggest, with production in Europe now 24% below 2017 levels. The downturn has taken capacity utilisation in Europe to just 55%, compared to 70% in 2019.

For the European manufacturers the main headache is competition from China, with Chinese players having 8% market share in the region. The Chinese are especially strong in electric vehicles (EVs) and hybrids which now account for 60% of new registrations in Europe. The Chinese combine good technology with low cost. In 2024, the former CEO of Stellantis estimated that BYD and other Chinese players had a 30% cost advantage over European manufacturers.

Europe reacted with tariffs, but in many cases these are not meaningful enough to dent sales. For instance, BYD is subject to a 27% European import tariff on EVs, but it is still able to offer its fully electric Dolphin Surf for just €23,000. Chinese players are also increasingly moving to plug-in hybrids as these are exempt from tariffs. In any case, tariffs will only be a short-term solution to Europe’s China problem. BYD plans to produce all its EVs for Europe locally by 2028. With their vertically integrated model, it is likely that BYD will continue to have a cost advantage as a local producer, but it will shrink as they lose scale benefits and take on a European labour force.

The problems for the European manufacturers extend beyond their home market. China has historically been a highly profitable market for them. Estimates are that before Covid it accounted for 40-50% of net income at Volkswagen, BMW and Mercedes. These profit pools are under enormous pressure, with Volkswagen reporting a drop in joint venture income from China of almost 80% in the first nine months of 2025, compared to 2019 levels. In the past the European manufacturers could point to superior quality and technology, but this perception is being challenged. The headwinds at home and abroad are reflected in operating margins for the European industry overall now at low single digit rates.

Sentiment is poor, with European autos in aggregate trading at just 0.6 times price-to-book. In the years before Covid, these companies have generated double digit returns on equity, but the market is now implying that they will never earn their cost of capital again.

Jean Monnet, a founding father of the EU, once said that “Europe will be forged in crisis, and will be the sum of the solutions adopted for those crises.” The same appears to be true for the continent’s auto manufacturers which are finally fighting back. They are now developing cars at “China speed”, implementing deep cost cuts, using better technology, and turning the joint venture model on its head. Below we will look at each of them in turn.

Speed. Historically it took European manufacturers four to five years to launch a new model. Volkswagen has recently announced that use of AI and simulation technologies allows them to reduce the product development cycle to two years. Renault achieved the same for its new Twingo. BMW argues that the modular architecture of their new platform allows them to launch 40 new models by 2027.

Costs. Estimates are that batteries account for 30-40% of an EV’s manufacturing costs, and these are coming down fast. BMW’s new platform is expected to have 40-50% lower battery costs, and it is the key driver for their ambition to achieve EV and combustion engine margin parity. Renault is transitioning to lower cost LFP batteries, supporting a 40% cut in total EV manufacturing costs. Europeans also benefit from falling costs as Chinese suppliers are adding massive amounts of battery capacity on the continent, with CATL alone having invested €11bn. Europeans are also adjusting their footprints, with Volkswagen having announced a 30% cut in their German workforce by 2030. Stellantis has idled capacity at several plants in 2025, and the company’s new CEO is expected to announce plant closures later this year.

Technology. European automakers are moving to centralised and zonal compute architectures, replacing dozens of separate control units. This makes software integration and software reuse across models much easier, and software is becoming a core product rather than an afterthought. They are also making great strides in battery performance, with new BMW and Mercedes models offering 700-800km range and charging times of 10 minutes for 350km. They are also becoming more competitive in the low‑price segment, with Volkswagen, Renault and Stellantis each preparing sub‑€25,000 EVs whose targeted ranges in many trims are broadly competitive with leading Chinese small EVs.

Partnerships. Historically, European manufacturers that wanted to produce in China were forced into joint ventures with local manufacturers who then copied their technology and ultimately leapfrogged them. While the EU does not exercise any force, the continent’s manufacturers are now keen on partnering with the Chinese to absorb their technology. Volkswagen is partnering with XPeng, jointly developing an EV architecture for the Chinese market, cutting both development time and manufacturing costs. Similarly, Stellantis announced a partnership with Chinese Leapmotor, combining Leapmotor’s low-cost EV technology with Stellantis’ global reach. Stellantis is also jointly investing in batteries with CATL.

As the examples above illustrate, the European manufacturers are on a good path, even if the reaction should have come years earlier. At this point, we are primarily invested through Exor, the holding company managed by John Elkann, which holds stakes in Ferrari and Stellantis. Using market values for underlying holdings where possible, Exor currently trades at a discount of over 50% to its net asset value. We have greater exposure to the automotive supplier space. The auto suppliers the funds are invested in trade at attractive valuations, have strong balance sheets, and, in our view, are not subject to the same disruption dynamics. These include Brembo, the global leader in premium brakes; Lear, the leading provider of luxury car seats; Elmos, a provider of automotive semiconductors; and Michelin and Hankook, both providers of tyres. All are powertrain-agnostic and operate at the premium end of the market, giving some protection from low-cost competition.

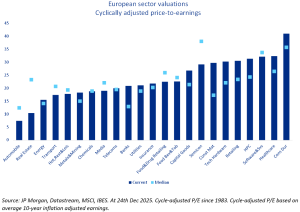

Autos are now the cheapest industry in Europe, with their cyclically adjusted price-to-earnings ratio at just 7.4. While not all manufacturers and suppliers will turn out to be winners, we believe a selective approach can uncover mispriced opportunities.

United Kingdom

United Kingdom United States

United States Canada

Canada