Away From the Casino Tables: The Wildest Value Gap Since 1999

Samuel Ziff

Partner | Portfolio ManagerSam Ziff joined OP in April 2013. He was previously employed by J.P. Morgan Cazenove working in the UK Industrials Corporate Finance team for a total of 4 years. He graduated from Oxford University. He is CIO, manages the global equity portfolios, and contributes to the overall investment selection.

The following insight piece was initially published by Investment Week and a link to the article can be found here.

Summary

US growth is more expensive than at almost any point in history, while deep value globally trades 45% below its 40-year median. The last time the gap was this wide, the crowded trade delivered a lost decade, and the forgotten corners of the market doubled.

When Warren Buffett recently described sentiment in markets, he said “The casino has gotten very attractive to people…. we’ve never had people in a more gambling mood than now.” You can see it in the numbers too: zero-day options, the lottery tickets of the investing world, now make up around 43% of daily volume, and retail traders explain more than half of this.

When market participants are gambling rather than investing, fundamentals like valuation become increasingly irrelevant. This may help explain why there has been only one other time in history, late 1999, early 2000, when the market was more expensive than today based on the Shiller price-to-earnings ratio.

Where is There Value?

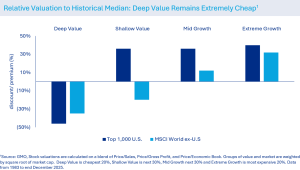

The chart below splits global equities into four valuation buckets, running from deep value to extreme growth, with each cohort’s current valuation shown as a premium or discount to its own 40-year median.

The cheapest bucket globally (“deep value”) trades at a 45% discount to its historical average, while extreme growth sits at a 40% premium. Shallow value outside the US remains meaningfully cheap. The further you move from US large-cap growth, the more likely you are to find something trading below its long-run valuation. This is the backdrop against which we invest.

We are often asked what kind of value investor we are: fundamental, deep, quality, or relative. We are both none and all of these. We go where value is most obvious, and that moves with the cycle. Wherever the discount is widest and the fundamentals are sound, that’s where we want to be.

What are the Implications for Investors’ Portfolios?

Benjamin Graham offered plenty of advice over the years, but one line feels especially apt today: “You can get in way more trouble with a good idea than a bad idea, because you forget that the good idea has limits.” Passive investing is a good idea, but the concentration and valuation risk embedded in the S&P 500 and MSCI World have quietly turned a global equity allocation into something it was never meant to be: a single, concentrated bet on the success of AI. Valuation is famously useless for timing; Greenspan coined ‘irrational exuberance’ more than three years before the bubble peaked, but it remains a powerful guide to long-run returns.

The last time markets were this concentrated and this expensive, the next decade belonged to the parts of the market the crowd had forgotten. From the end of 1999 to the end of 2009, the MSCI World and S&P 500 delivered close to a zero total return, while emerging markets doubled and value outperformed growth. The Overstone Global strategy delivered 6% annualised over this period, with 30bps of outperformance in up months and 80bps in down months2. A globally diversified, valuation-aware portfolio didn’t just outperform; it was the difference between a lost decade and a good one.

This is the world our global value fund is built for. We have been meaningfully underweight US equity for some time, with the portfolio focused on companies trading at deep discounts to their long-run multiples. That positioning has been a headwind through the AI rally; we do not pretend otherwise. But the conditions that have made it painful are the ones that historically precede strong relative performance.

The casino may stay open a while longer. However, the best returns over the next decade are unlikely to come from the tables everyone is crowded around.

2Source: OP and MSCI ©

United Kingdom

United Kingdom United States

United States Canada

Canada